This is the fifth blog in a new series of blogs that focuses on Article 7’s Right to Information requirement. Access the previous installments below:

- Blog 1: Challenges and How to Ensure Compliance

- Blog 2: Response Deadlines and Annual Worker Notification Requirements

- Blog 3: How Member States Are Addressing Privacy and GDPR Considerations

- Blog 4: How Right to Information Could Drive Equal Pay Claims Across Entities

When the EU Pay Transparency Directive defines “pay,” it casts a remarkably wide net. Article 3(1)(a) covers “the ordinary basic or minimum wage or salary and any other consideration, whether in cash or in kind, which a worker receives directly or indirectly (complimentary or variable components) in respect of his or her employment from his or her employer.”

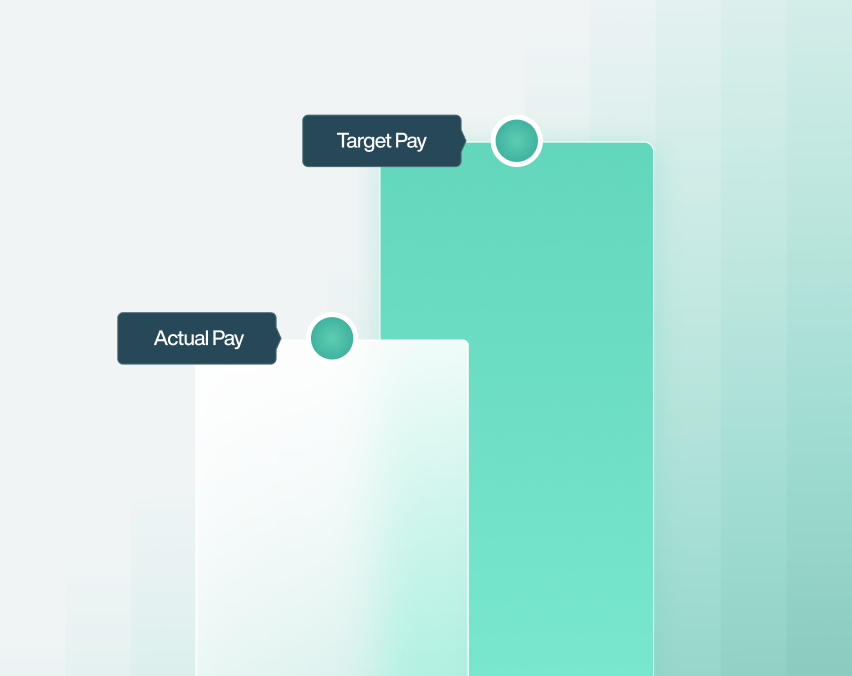

That breadth creates two immediate operational challenges for multinational employers: first, it points unmistakably toward actual pay received rather than target or budgeted compensation; and second, the precise boundary of what belongs in that calculation is being drawn differently across the 27 member states.

Actuals, Not Targets

The phrase “which a worker receives” is backward-looking by design. The Directive is asking what was paid, not what was budgeted, graded, or planned. That distinction matters enormously for data architecture.

Most HR information systems hold the forward-looking view: salary grades, target bonus percentages, job-level pay bands. Payroll systems hold the actuals. Compliant Right to Information (RTI) responses and pay gap reporting will require drawing from both and reconciling them.

Czechia’s explanatory notes make this explicit, requiring that RTI data be “up-to-date and objectively quantifiable” while ensuring that remuneration components not provided regularly and other monetary benefits and benefits of monetary value are also captured. That is a clear instruction to go beyond the HRIS and into payroll records.

Denmark and Finland have cut through the ambiguity by anchoring reporting to existing payroll data flows. Denmark is tying reporting to Statistics Denmark Act submissions, which capture actual earnings including base salary, bonuses, pension contributions, taxable benefits such as company cars and health insurance, and actual hours worked. Finland plans to leverage its real-time Incomes Register, where employers already report every payment transaction — salaries, fringe benefits, fees, and cost reimbursements — at the individual level.

For employers operating in those markets, the data source is clear. For everyone else, the answer is being written in transposition legislation right now.

Where the Definitions Diverge

The Directive’s breadth has not produced uniform national definitions. Member states are making meaningful choices — and some of those choices create compliance tension with the Directive itself.

Broadly Inclusive Approaches

- The Netherlands clarifies in its explanatory notes that “pay” should include base pay, as well as key additional components commonly found in payroll, such as bonuses, overtime compensation, and private car use. Components not tracked at the individual level — such as items recorded under the work-related costs scheme (company parties, work clothing) — are not expected to be included.

- Slovakia’s earlier legislative draft carved out statutory entitlements — benefits to which employees are legally entitled and whose amounts are not subject to employer discretion — from the definition of pay. That carve-out was removed in the final published legislation, in favor of the broad definition of “pay” more in line with the Directive.

Narrower or Contested Approaches

- Italy specifically includes continuous and fixed remuneration elements, while excluding non-structural individual economic benefits from its definition of “pay level” — specifically, pay components recognized on a personal, discretionary, or temporary basis that are not generalized across a worker category and are based on individual objective criteria. The explanatory notes identify individual superminimums, one-off bonuses, and ad personam allowances as examples of excluded items. Italy’s potential exclusion of one-off bonuses could be interpreted as being at odds with the Directive, since these are precisely the areas where discriminatory practices can most easily take root.

- Latvia includes salary plus allowances, bonuses, and any other work-related remuneration — provided it is paid on a regular basis. Latvia adds this “regularity” condition but does not provide guidance on how to assess it.

- Poland defines the remuneration level as gross annual and hourly remuneration, excluding only benefits that are universally available to all employees within a category with no conditions attached to their use, as well as benefits related to the termination of the employment relationship (e.g. severance pay).

- Germany’s commission report recommended that it should be possible to exclude voluntary optional benefits and benefits not granted by the contractual employer, such as stock options and phantom stocks.

Still Awaiting Lower-Level Guidance

Many Member States have clarified that additional guidance will be provided in secondary legislation or guidance. For example, Czechia’s Ministry of Labour and Social Affairs will establish by decree the method for calculating remuneration and other monetary benefits required under RTI. France will define by decree the calculation methods and the elements of remuneration to be taken into account. Lithuania’s Ministry of Social Security and Labour must adopt implementation acts by June 6, 2026.

What’s Generally In — and What’s Contested

Based on transposition drafts and explanatory notes to date, the following pay components are broadly expected to be included:

- base salary

- regular bonuses

- overtime compensation

- taxable benefits such as company cars and health insurance

- pension contributions

- fringe benefits,

- allowances set out in collective agreements or employment contracts.

Components that are excluded or contested in at least some jurisdictions include:

- work-related cost reimbursements not tracked at the individual level (Netherlands),

- one-off bonuses and ad personam allowances (Italy decree),

- Universally available and unconditioned benefits (Poland draft),

- Benefits related to termination (Poland draft)

- and voluntary optional benefits and discretionary equity instruments such as phantom stock (Germany commission recommendation).

What Employers Should Do Now

The definitional variation across member states is not a reason to wait. The underlying data challenge — bridging HRIS records and payroll actuals — is universal, regardless of where national lines eventually land. Employers that have already mapped their pay data architecture will be better positioned to adapt as lower-level guidance emerges.

Three actions are worth taking now.

- Audit the gap between what lives in your HRIS and what is captured in payroll systems. Non-cash benefits, individually negotiated allowances, and irregular payments often fall into this gap.

- Identify which pay components are tracked at the individual level versus in the aggregate — the Netherlands has made this distinction explicit, and other countries likely will too.

- Model the data impact of both inclusive and exclusive definitions for high-ambiguity components like one-off bonuses and discretionary allowances.

The Directive’s intent is clear even where the national definitions are not: discretionary, individually negotiated pay is precisely where transparency is most needed. Employers that build toward that intent — rather than toward the narrowest available definition — will face fewer surprises as guidance matures.

Definitional clarity will sharpen considerably as countries with pending decrees publish their calculation methodologies and additional guidance.

How Trusaic Is Helping Clients Comply with Right to Information Requests

At Trusaic, we are helping employers move from reactive compliance to scalable readiness.

First, organizations conduct a defensible pay equity analysis through PayParity®. This ensures that total remuneration is analyzed, unjustified gaps are identified and remediated using R.O.S.A., and ready for RTI disclosures. A validated pay equity analysis can provide confidence and a clear understanding of risk as companies begin RTI compliance.

Second, we enable automated RTI workflows. Our bi-directional integrations with global HCM platforms allow pay equity data to flow securely from the Trusaic platform back into the HCM. Employees can then access their RTI reports directly within their existing HR systems. This eliminates manual report generation and reduces compliance risk.

For organizations that prefer platform-based access, RTI reports can also be generated and delivered securely through the PayParity platform, with role-based permissions and full auditability.

Reports can be generated instantly, refreshed regularly, and delivered in any EU language — easing the operational strain on organizations.

Finally, our expert advisory team will assist you in constructing your contextual narratives alongside RTI reports. (Note: Employers also have the option to utilize our in-platform AI-powered contextual narrative support). Rather than presenting raw pay data without explanation, organizations can configure tailored narratives that reflect their pay philosophy and clarify wage-influencing factors. For large enterprises anticipating thousands of RTI interactions, this significantly reduces administrative burden while improving employee understanding.

Organizations that partner with us will not only be supported in meeting Directive’s requirements — they will enter this new transparency landscape with confidence and credibility.

Visit our always updated Member State Transposition Monitor to stay on top of the latest EU Pay Transparency Directive developments.