In December, two pieces of legislation were passed that affected ACA compliance for the 2024 tax year onward.

We broke down the full impact of the Employer Reporting and Improvement Act and Paperwork Burden Reduction Act in a previous blog. The Paperwork Burden Reduction Act enabled employers to notify employees of their right to access 1095-C forms instead of mailing it to them, which was previously required.

The IRS recently issued guidance regarding this rule for the 2024 tax year. Employers that opted to provide employees form only upon request must ensure their notification remains accessible on the company website through Oct. 15, 2026.

In this blog, we’ll break down the specifics of the rule as it relates to IRS guidance.

What’s Changed in the Employee Notification Requirement?

The Paperwork Reduction Act amends Section 6056 of the Internal Revenue Code, which obligates ALEs and health insurers (carriers) to prepare and furnish Forms 1095-C/1095-B to employees. ALEs are no longer required to mail forms to employees if they meet certain requirements.

Employers can instead opt to provide these forms only upon employee request, provided they meet certain conditions:

- Employee notification: Employers must provide clear, conspicuous, and accessible notice to employees, informing them of their right to request Form 1095-C.

- The new guidance dictates that this must remain on the company website until Oct. 15, 2026.

- Timely furnishing upon request: Upon receiving a request, employers must furnish the employees Form 1095-C by the later of:

- March 2 (previously Jan. 31) of the year following the calendar year in which coverage was provided, or

- 30 days after the date of the request, whichever is later.

This update aligns with the broader transition to electronic ACA filing, which became mandatory for virtually all employers beginning with the 2023 tax year.

Why It Matters

Failure to comply with ACA employee notification requirements can trigger penalties under IRC Sections 6721 and 6722, which govern failures to file or furnish information returns correctly.

Key risks include:

- Employee complaints or confusion, especially during tax filing season.

- IRS inquiries or audits triggered by non-compliance with notification timelines.

- Loss of eligibility to furnish forms electronically if consent and communication rules are not followed.

To remain compliant with the new guidance, employers should:

1. Review Your Electronic Furnishing Process

Confirm that your organization has properly obtained consent from employees to receive Form 1095-C electronically and that your communication process includes the required notice.

2. Update Internal Web Content

Ensure your company’s intranet or employee portal includes a clear and accessible notification that:

- Describes the employee’s right to request a paper copy of Form 1095-C

- Explains how to request the form

- Stays visible on the site through Oct. 15, 2026

3. Work With HR and Legal to Ensure Compliance

Coordinate with your HR, payroll, and legal teams to document this process and verify that all ACA compliance communication materials align with the latest IRS rules.

Challenges and Considerations for Employers

While the new 1095-C furnishing rule seems simple in theory, we believe it could introduce significant compliance challenges. Thus, employers should be aware of a few complications that could arise:

- Tracking issues: If employees request their 1095-C form, how will you keep track of those instances? Without a formalized furnishing process in place, you risk data inconsistencies over time. The burden of proof falls on the employer to establish compliance for seven years after a form has been furnished.

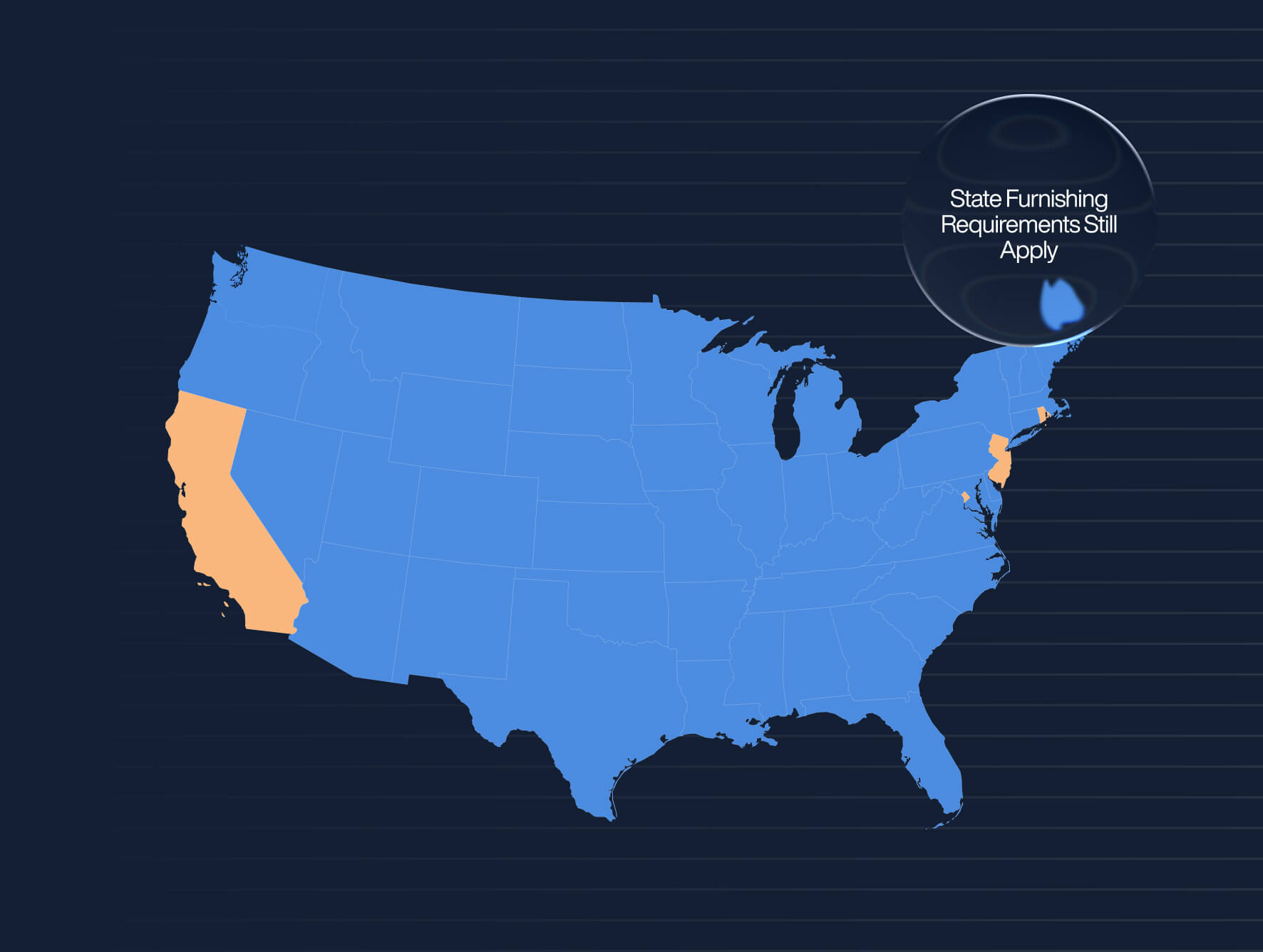

- State ACA requirements: If an employee lives in or moves to a state with its own ACA requirements and never received a 1095-C form during a specific tax year, you could be out of compliance with that state’s furnishing requirements. Of the four jurisdictions — California, New Jersey, Rhode Island, and Washington D.C. — that have implemented their own individual mandate and separate Employer ACA filing and furnishing requirements, only one, Washington D.C., has specific guidance that says compliance with federal distribution standards satisfies that jurisdiction’s furnishing requirement.

- Employee turnover: Every employer has turnover. If you utilize the “upon request” method, it becomes more difficult to track and manage when 1095-C forms were furnished and to whom, which becomes an unnecessary compliance risk over time.

The deadline for the 2024 tax year has passed, but the surface-level simplicity of the “by request” option could appeal to employers in 2025. Thus, it’s important to be cognizant of the various compliance challenges it could create.

How Trusaic Simplifies Compliance

Trusaic’s ACA compliance service enables you to offload 1095-C furnishing and filing responsibilities. Our designated support team prepares and distributes your 1095-C forms on-time to applicable employees by U.S. mail or electronically on demand.

Given the new legislation, we offer our clients two options to choose from:

- e-Distribution + Print and Mail (CA, RI, NJ only)

- Print and Mail only

Option 1 is our recommended approach and organizations can e-distribute with ease utilizing Trusaic’s platform. Our e-distribution platform makes it easy for an employer to notify their employees of the option to receive their forms while providing them with a link where they can access the form electronically.

This also simplifies any employee follow-up requests for a form as the employer can simply resend the link to their employee giving them digital access to their forms. This ensures all your forms are distributed on-time and can be easily tracked for compliance purposes.

Book a meeting to learn how other companies are adopting this approach to Form 1095-C furnishing for next year.