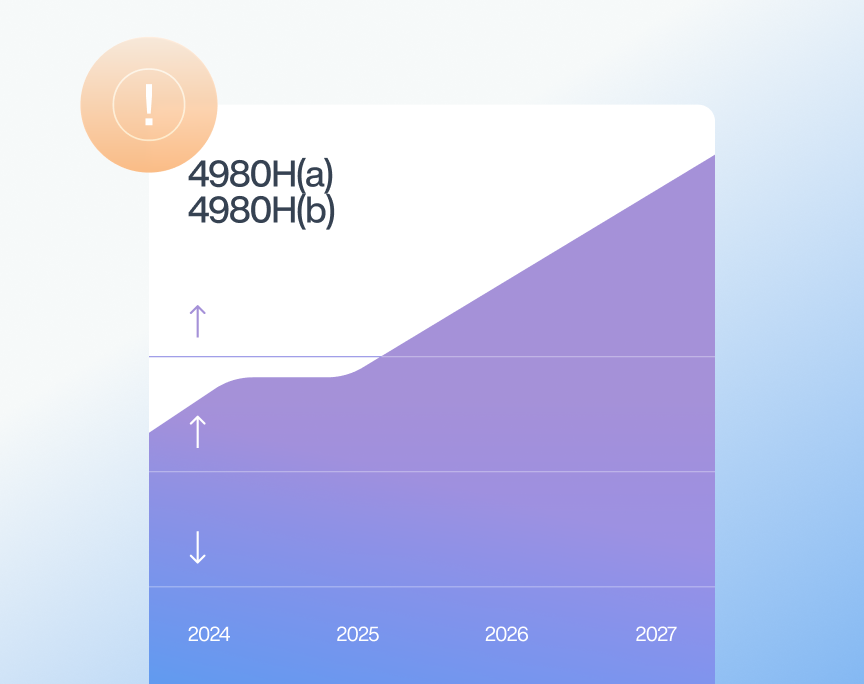

The IRS has officially released two core ACA compliance benchmarks for 2027: inflation-adjusted ESRP penalty amounts and a new all-time-high affordability percentage of 10.22% under Code Sec. 36B — the highest required contribution threshold since the employer mandate took effect. Both figures are now final, and both require updated calculations before plan year enrollment begins.

Protecting your organization against these rising penalty assessments requires more than simply offering health insurance. It demands accurate affordability calculations, clean data reporting, and an audit-ready compliance posture.

How Much Are the 2027 ACA Penalties Increasing?

The 4980H(a) Penalty (“A” Penalty)

- 2027 Amounts: $3,780 annually / $315.00 monthly.

- The Trigger: This penalty applies if an Applicable Large Employer (ALE) fails to offer Minimum Essential Coverage (MEC) to at least 95% of its full-time workforce and their dependents, and at least one full-time employee receives a Premium Tax Credit (PTC) from an exchange.

- Year-Over-Year Increase: The 2027 rate is up from $3,340 annually ($278.33/month) in 2026 — a $440 increase that continues the consistent upward trajectory of ESRP assessments.

The 4980H(b) Penalty (“B” Penalty)

- 2027 Amounts: $5,670 annually / $472.50 monthly.

- The Trigger: This is assessed if the ALE meets the 95% offer threshold, but fails to offer affordable or Minimum Value (MV) coverage to specific full-time employees who subsequently receive a PTC.

- Year-Over-Year Increase: The 2027 rate is up from $5,010 annually ($417.50/month) in 2026 — a $660 increase that compounds the per-employee risk exposure for ALEs with affordability gaps in their coverage offerings.

What Is the 2027 ACA Affordability Percentage?

For plan years beginning in calendar year 2027, the IRS has set the required contribution percentage at 10.22% under Code Sec. 36B — the highest affordability threshold in ACA history.

This figure determines whether employer-sponsored coverage qualifies as affordable: if an employee’s required contribution for self-only coverage exceeds 10.22% of the applicable safe harbor measure, that employee may qualify for a Premium Tax Credit, which is the trigger for a 4980H(b) penalty assessment.

How Does the IRS Calculate Your Corporate Risk Exposure?

The IRS enforcement process is automated via the IRS AIRS System. This means penalties are triggered by data syntax errors and form mismatches, not necessarily by human auditors.

The 4980H(a) penalty scales aggressively. If triggered, it is applied to the entire full-time workforce minus the first 30 standard exemption, rather than just the single employee who received a PTC.

Because of this scaling, ensuring accurate Form 1094-C and Form 1095-C reporting is critical to your corporate risk management strategy.

The Escalation of Letter 226J

When an organization operates with a disconnected HRIS and payroll stack, coding inconsistencies can trigger an IRS Letter 226J assessment. Consider the financial impact of a systemic 4980H(a) error for the 2027 reporting year:

- The Scenario: An ALE with 500 full-time employees incorrectly codes Form 1094-C, suggesting they failed to meet the 95% MEC offer threshold.

- The Trigger: One employee visits an exchange and receives a PTC.

- The Assessment: The IRS calculates the 2027 “A” Penalty ($3,780) across the workforce minus 30 employees (470).

- The Liability: The automated Letter 226J proposes an Employer Shared Responsibility Payment (ESRP) of $1,776,600.

How Fragmented Data Multiplies Your IRS and State Liability

Disconnected HRIS, payroll, and benefits systems create data that triggers regulatory flags. When systems do not communicate, employers face compounding risks:

- Federal Syntax Errors: Misclassified variable-hour employees and mismatches between Line 14 and Line 16 of Form 1095-C are the primary drivers of automated IRS penalties.

- State-Level Discrepancies: Jurisdictions with individual mandates (like California and New Jersey) require state filings that perfectly mirror your federal transmittal. Discrepancies between IRS and state submissions are immediate red flags for auditors.

- Missed Safe Harbors: Siloed payroll data often prevents the accurate, proactive application of affordability safe harbors, artificially inflating your perceived penalty liability.

A Proactive ACA Solution for Employers

Navigating the nuances of the tax code and these rising penalty amounts requires specialized regulatory expertise, not just standard out-of-the-box payroll software.

Trusaic’s ACA Complete® provides a centralized, high-integrity solution that acts as your single source of truth. We ensure that every record transmitted to the IRS AIRS System is forensic-grade and fully audit-ready.

Partnering with Trusaic gives your organization access to:

- Pre-Filing Data Validation: Catch and resolve Form 1094-C and 1095-C coding errors before IRS AIRS transmission.

- Seamless Regulatory Transmission: Automated formatting and filing for both federal IRS requirements and state mandates.

- Dedicated Penalty Defense: Full audit support and regulatory expertise to eliminate proposed assessments.