While HR and benefits teams are currently focused on finalizing reporting for the current filing season, the IRS offered a reminder that it’s still actively enforcing prior years. The agency has begun issuing Letter 226J penalty assessments for the 2023 tax year.

The IRS enforcement mechanism is moving quickly. The agency began issuing Letter 226J notices for the 2022 tax year in November 2024, and has shifted its focus to 2023. If an organization receives a Letter 226J for 2023, it means the IRS system found a mismatch between the organization’s 1095-C filings and its employees’ tax returns.

What Is Letter 226J?

Treat Letter 226J as an urgent alert that the IRS has found a data discrepancy in your filings. This assessment is automatically generated when the IRS cross-references your 2023 1095-C filings against individual tax returns and finds a mismatch.

Specifically, if one of your full-time employees received a Premium Tax Credit (PTC) on a state or federal exchange, the IRS system infers that your organization failed to offer affordable, minimum value coverage, triggering a proposed Employer Shared Responsibility Payment (ESRP).

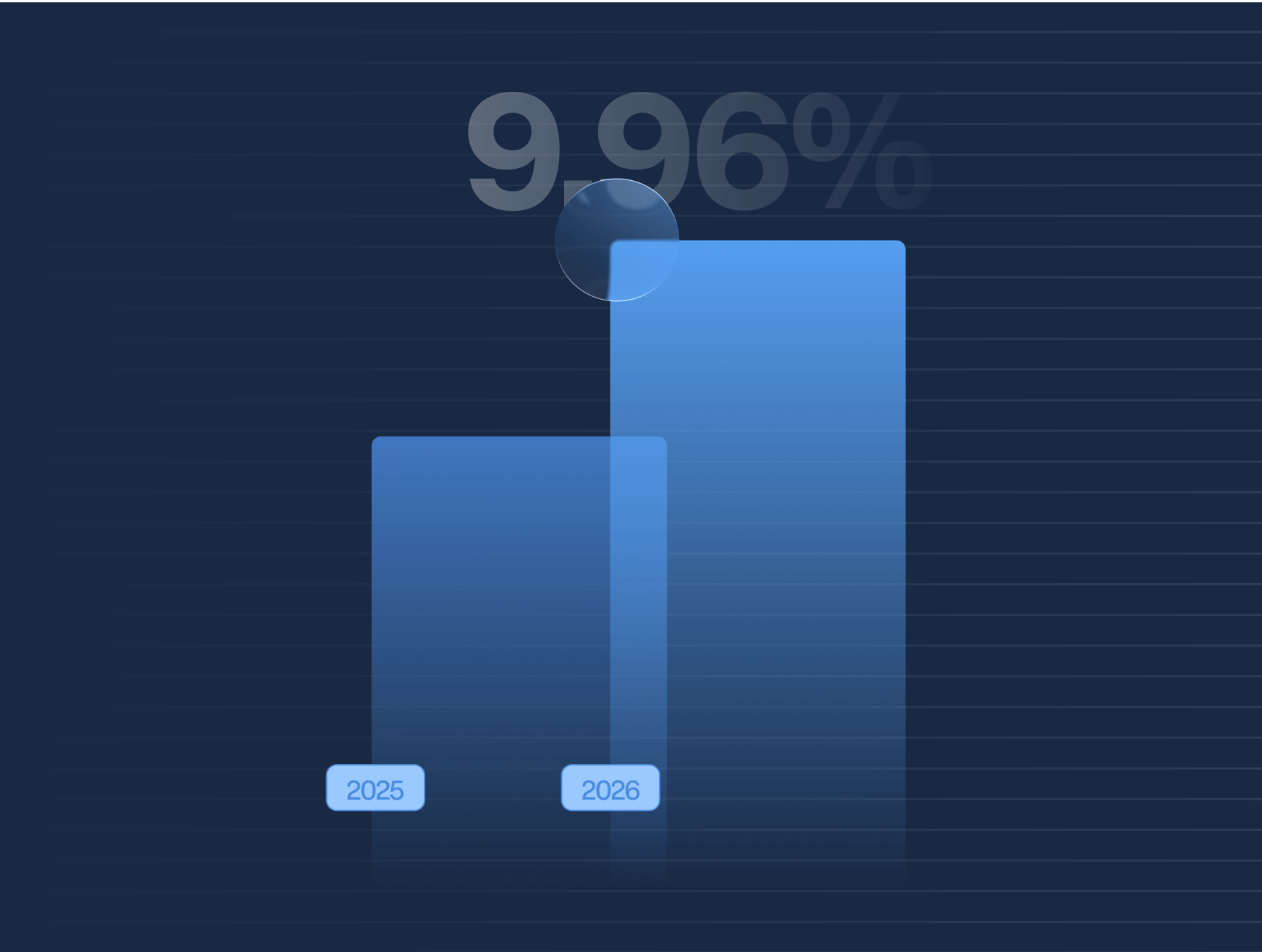

Understanding 2023 Penalty Exposure

ACA penalties are indexed annually for inflation, meaning the cost of non-compliance varies by tax year. For 2023, the financial stakes are specific and significant:

- A Penalty (Failure to Offer): For 2023, the Section 4980H(a) penalty is $2,880 per employee (annualized).

- Often referred to as the “Hammer Penalty,” this is assessed if an ALE fails to offer Minimum Essential Coverage (MEC) to at least 95% of its full-time workforce, and at least one full-time employee receives a PTC. It is calculated based on the entire full-time workforce (minus the standard 30-employee exemption), not just the employees who received credits.

- B Penalty (Failure to Offer Affordable/Minimum Value): For 2023, the Section 4980H(b) penalty is $4,320 per employee (annualized).

- This applies if an employer offered coverage to 95% of its workforce, but a specific employee received a PTC because their offer was unaffordable or didn’t meet Minimum Value. It is assessed only on the specific employees who received a tax credit.

The 2023 Affordability Blind Spot

A critical area of exposure for the 2023 tax year involves the specific affordability percentage used for Safe Harbor calculations.

For 2023, the IRS lowered the affordability threshold to 9.12% (down from 9.61% in 2022).

If plan premiums remained static from 2022 to 2023 while the threshold dropped, coverage may have drifted out of the Safe Harbor zone. This gap is a primary driver for the B Penalty assessments appearing in this current wave of letters.

What To Do If You Receive a Notice

Receiving a Letter 226J does not automatically indicate that payment is owed. A significant portion of these proposed penalties results from simple coding errors, like omitting a 2C code for employee enrollment, rather than actual non-compliance.

However, organizations must act quickly. The IRS provides a response window, 90 days from the date of the letter.

- Review Form 14765: This attachment lists the specific employees who triggered the penalty. Cross-reference this list immediately with 2023 payroll and benefits data.

- Audit the Codes: Examine lines 14 and 16 of the 1095-C for the flagged employees. Was the correct Affordability Safe Harbor used? Was a Limited Non-Assessment Period accurately reflected for a new hire?

- Prepare a Defense: Employers must formally disagree with the assessment using Form 14764 and provide supporting evidence to correct the record.

Trusaic Can Defend Against Letter 226J

Navigating an IRS inquiry requires precision. It is necessary to prove not just that coverage was offered, but that it was reported correctly according to the 2023 statutes.

If your organization has received a Letter 226J for the 2023 tax year, assistance is available. Trusaic’s IRS Penalty Response Service helps employers audit historical data, identify the root cause of the discrepancy, and draft the necessary response to the IRS to reduce or eliminate the assessment.

We’ve saved our clients more than $1 billion in penalties, with many achieving reductions of 90% or more.

Don’t pay a penalty you don’t owe, schedule a Letter 226J review with Trusaic today.