The Affordable Care Act (ACA) introduced a wide range of compliance obligations for employers, particularly under the Employer Mandate.

These responsibilities can often feel overwhelming, especially as rules evolve and penalties increase. To help simplify, we’ve compiled a list of the most common questions employers have about the ACA Employer Mandate and reporting requirements and how Trusaic can help ensure compliance.

What Is the ACA Employer Mandate?

The ACA’s Employer Mandate requires Applicable Large Employers (ALEs) — organizations with 50 or more full-time employees, including full-time equivalents — to offer affordable, minimum essential coverage that meets minimum value standards to at least 95% of their full-time employees and their dependents.

Failure to do so can result in IRS penalties under IRC Sections 4980H(a) and 4980H(b).

Who Qualifies as a Full-Time Employee Under the ACA?

For ACA purposes, a full-time employee is anyone working at least 30 hours per week or 130 hours per month. Employers must use IRS-approved measurement methods such as the monthly measurement or look-back measurement to determine eligibility.

What Are the Penalties for Non-Compliance?

The penalties can be significant:

- 4980H(a): Applies if an ALE fails to offer coverage to 95% of full-time employees. For the 2025 tax year, the penalty is $2,900 annually per full-time employee (minus the first 30 employees).

- 4980H(b): Applies if coverage is offered but is unaffordable or doesn’t meet minimum value. For 2025, the penalty is $4,350 annually per employee receiving subsidized coverage on the Marketplace.

What Reporting Is Required Under the ACA?

Employers must file and furnish two key forms:

- Form 1094-C: Transmittal form submitted to the IRS summarizing coverage information.

- Form 1095-C: Filed with the IRS and furnished to employees, detailing coverage offered, employee status, and affordability information.

Some states — including California, Rhode Island, New Jersey, Massachusetts, and Washington, D.C. — have their own ACA reporting mandates in addition to federal requirements.

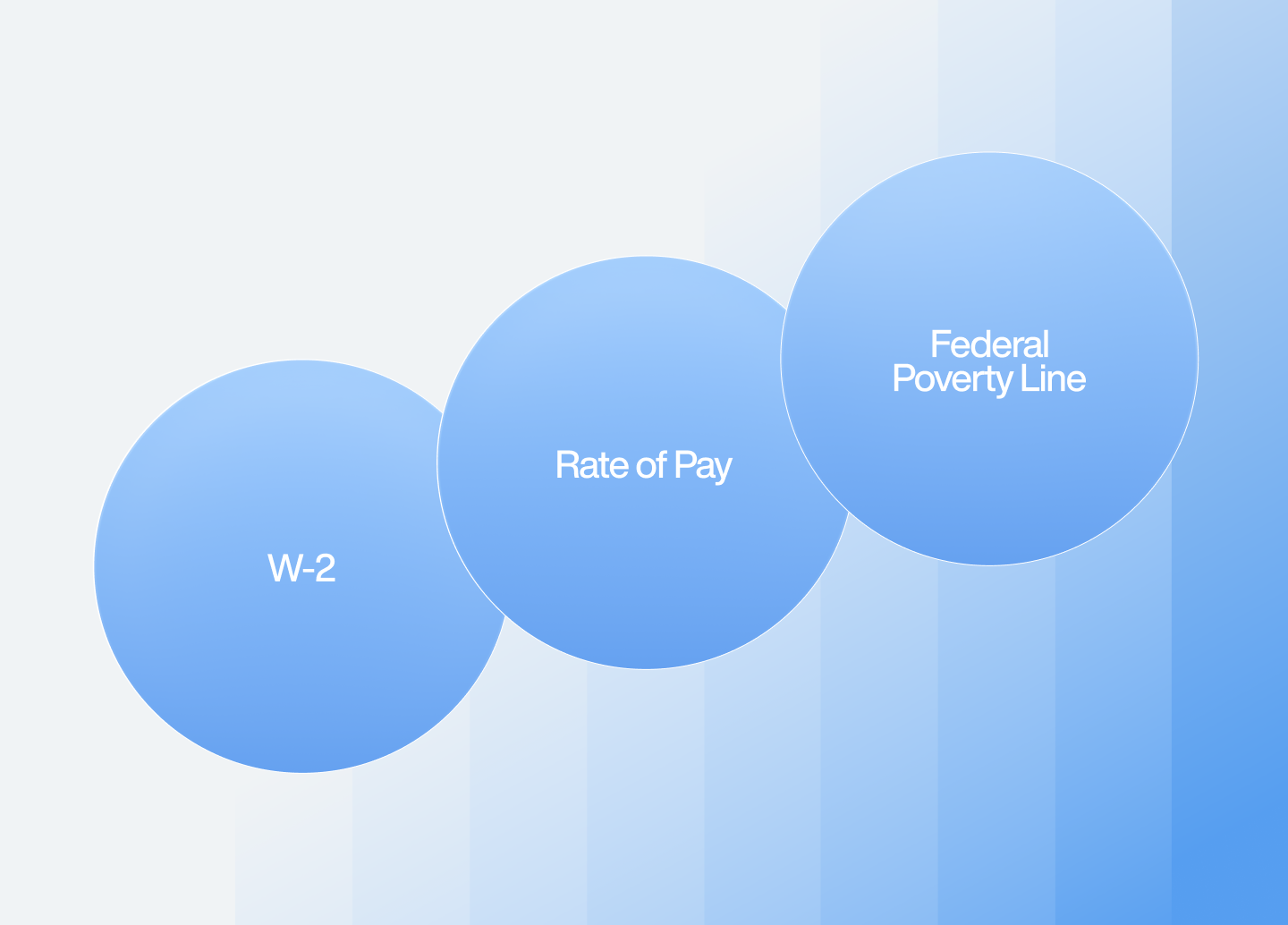

What Are Affordability Safe Harbors?

The IRS provides three “safe harbor” methods for employers to demonstrate affordability:

- W-2 Safe Harbor

- Rate of Pay Safe Harbor

- Federal Poverty Line (FPL) Safe Harbor

Employers may choose the method that best aligns with their workforce structure to avoid penalties under Section 4980H(b).

How Does the IRS Enforce ACA Compliance?

The IRS identifies potential non-compliance through reporting discrepancies and issues penalty notices, such as:

- Letter 226J – Notifies ALEs of proposed Employer Shared Responsibility Payments.

- Letter 5699 – Requests missing filings when the IRS suspects non-filing.

Employers must respond promptly to avoid automatic penalty assessments.

What Tools Are Available to Help with ACA Compliance?

ACA compliance is not just about meeting filing deadlines. It’s about ensuring your coverage, reporting, and documentation are accurate year-round. With the IRS actively issuing penalty letters and new state-level requirements emerging, the risk of non-compliance is higher than ever.

Trusaic’s ACA Compliance Solutions provide:

- Penalty Risk Assessment – Identify compliance gaps before IRS penalties arise.

- Ongoing Monitoring – Track full-time employee status, affordability, and eligibility throughout the year.

- Seamless Integrations – With HCM systems like Workday, UKG Ready, and more.

- Audit Defense – Support for responding to IRS inquiries with legally defensible data.

- Federal and State Filing – Automated preparation and submission of Forms 1094-C and 1095-C.

By leveraging Trusaic’s ACA Compliance Solutions, employers can simplify the complexity, mitigate risks, and ensure they remain compliant with confidence.