Receiving an IRS notice is stressful. Receiving a Notice of Intent to Levy is an operational crisis.

For many employers, this crisis stems from a simple administrative oversight that spirals out of control. A missed ACA filing deadline triggers an automated IRS inquiry (Letter 5699), which escalates to a proposed penalty (Letter 5005-A), hardens into a bill (Letter 972CG), and finally results in a threat to seize assets.

We recently stepped in to assist an organization facing this exact scenario. Their experience highlights a critical lesson for every employer: The IRS’s initial assessment can be wrong, but the burden of proof is on you.

Why the IRS Overestimates Liability: The W-2 Headcount Error

When an organization fails to file ACA returns, the IRS has to estimate their liability. Typically, the agency looks at W-2 filings to estimate the workforce size.

In this specific instance for our client, the IRS saw over 300 W-2s filed for the year. Consequently, they assessed a massive failure-to-file penalty based on an assumption that the organization had 300 full-time employees.

This is a common data misconception. The ACA Employer Mandate does not penalize you based on your total headcount; it penalizes you based on your full-time workforce.

The Defense Strategy: Forensic Data Analysis

The organization turned to Trusaic’s Penalty Letter Response to address the levy process. Our first step was not legal argument, but data forensics.

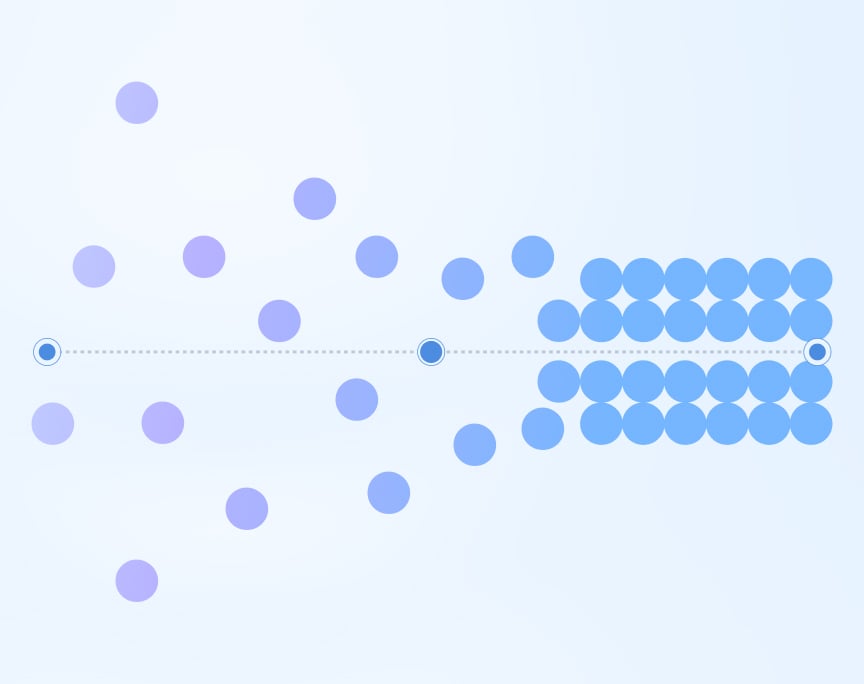

By performing a retrospective audit of their payroll and benefits data, we identified that despite having 300+ employees, the organization’s actual full-time equivalent (FTE) count was between 50 and 60. The vast majority of their workforce consisted of variable-hour, part-time staff who did not trigger penalty liability.

However, simply telling the IRS “you are wrong” is not enough. There is a rise in the IRS requesting signed statements breaking down monthly full-time counts, alongside the specific payroll records and calculation methodologies used to justify every employee’s classification.

Required Documentation: Proving Employee Status to IRS Auditors

To overturn the assessment, we had to reconstruct the past. We submitted the delinquent filings along with a comprehensive evidence package that validated the lower employee count. This defense relied on three pillars of data:

- Raw Time and Attendance Data: We processed historical payroll logs to prove the actual hours of service for the variable-hour workforce, distinguishing part-time staff from full-time.

- Measurement Period Analysis: We documented the specific Look-Back measurement periods established for that tax year, validating that the employees in question were correctly classified during their stability periods.

- Benefits Offer Substantiation: We cross-referenced benefits enrollment data to prove that the 50–60 legitimate full-time employees were offered compliant coverage.

The Result: Reducing Liability to 2% of the Assessment

Data is the ultimate defense. The IRS’s initial assessment relied on a broad W-2 headcount, but our forensic data analysis revealed the operational reality: most of those employees were variable-hour workers who did not trigger coverage mandates.

By correlating raw time-and-attendance logs with precise measurement periods, we mathematically proved that the company’s actual liability was a fraction of the IRS’s estimate. This evidence-based approach allowed us to submit a request reducing the penalty to approximately 2% of the original levy amount.

How to Stop an IRS Intent to Levy

The most dangerous action an employer can take is inaction. The IRS automated compliance system interprets silence as an admission of liability. If you have received a Letter 5699 or a Letter 5005-A, the clock is counting down toward a levy.

However, as this case demonstrates, even a six-figure assessment can be reduced with the right evidence. You do not have to accept the IRS’s initial calculation as the final word.

Trusaic does more than just file forms; we defend them against the highest levels of IRS scrutiny. If you are facing an assessment, do not wait for the proposal to become a seizure. Contact us today to verify your liability and build your data-backed defense.