In the fast-paced environments of retail, food service, and hospitality, a significant portion of the workforce exits the organization passively: they stop showing up for their scheduled shifts.

When a worker abandons a position without filing formal separation paperwork, a dangerous data lag develops between the storefront and the centralized corporate HRIS. These individuals become “ghost employees” — lingering on the active payroll roster with zero hours and zero wages.

For Applicable Large Employers (ALEs), this disconnect is more than an administrative headache; it is a cause of Form 1095-C coding failures that trigger automated IRS penalty assessments.

The Downstream Impact of Delayed HRIS Termination Entry

The IRS AIR System requires data accuracy on every Line 14 and Line 16 entry of Form 1095-C. When a departed employee remains in an active state within an unintegrated database, it skews payroll records and generates false compliance signals.

This data fragmentation introduces three distinct vulnerabilities into your corporate risk management strategy:

- Corrupted Affordability Math: Keeping non-working, zero-wage employees as active skews your workforce FT counts, potentially confusing FTE calculations and overinflating FTE counts. The calculation is no longer looking at true employees – it is inaccurately including employees who have already left.

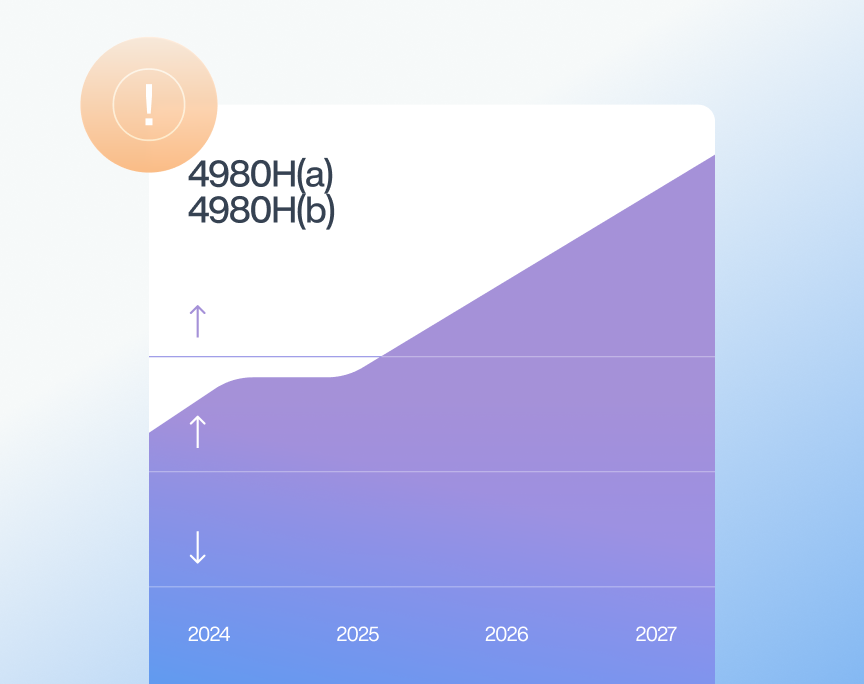

- Conflicting Form Coding: Line 14 may indicate a valid offer of coverage was made, but Line 16 will lack the proper code (such as 2C for enrolled, or a valid safe harbor) because the individual has abandoned the job. The missing safe-harbor or enrolled code leaves the employer exposed to 4980H penalties.

- Multi-Month Exposure: The longer a departed worker lingers on the active roster without an official termination date, the larger the 4980H penalty exposure due to missing safe-harbor or enrolled codes.

How a Delayed Termination Entry Triggers Letter 226J

Failing to maintain real-time synchronization between store-level termination and enterprise databases could cause financial consequences.

- The Scenario: A fast food restaurant team member walks off the job in mid-October during a pre-holiday peak. The store manager fails to process the formal separation paperwork until January.

- The Data Gap: For three months, the corporate HRIS shows an active full-time employee with 0 hours and no offer of coverage; resulting in a “1H/” code (no offer/no explanation).

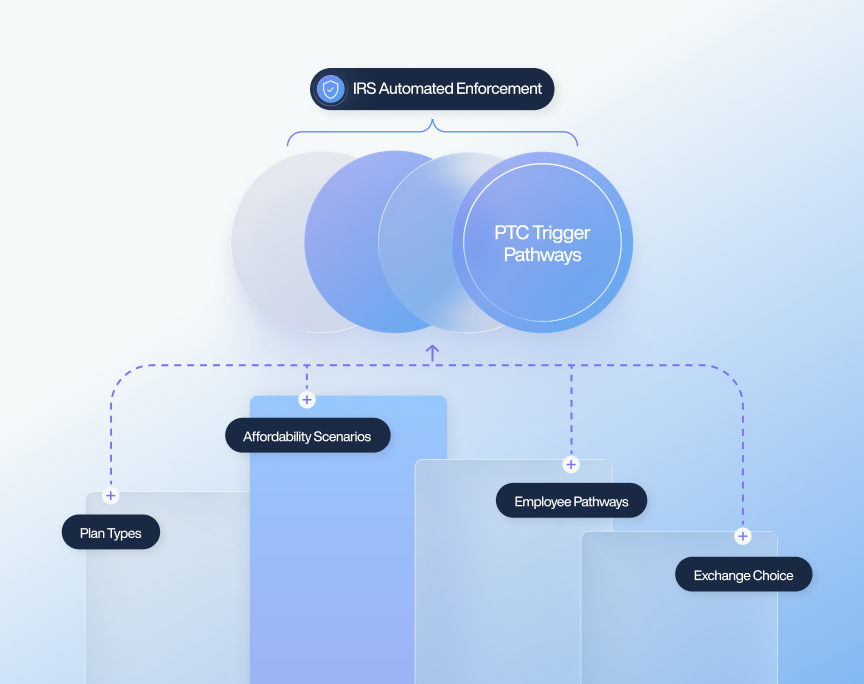

- The Audit Scan: The former employee applies for subsidized health insurance on an exchange for November and December, securing a Premium Tax Credit (PTC).

- The Assessment: The IRS AIR System scans the employer’s year-end filing, flags the unapproved coverage gap during those active employment months, and issues an automated Letter 226J ESRP.

The Q1 Challenge: Cross-Departmental Friction

When year-end reporting deadlines arrive, siloed systems can trigger a corporate firefight. Corporate compliance teams suddenly discover massive discrepancies between W-2 wage lists, active benefits enrollments, and active HR rosters.

Because the data is decentralized, a cycle of internal finger-pointing begins:

- Operations blames store-level managers for failing to submit physical paperwork on time amidst high holiday turnover.

- HR blames payroll for keeping inactive workers on the roster or failing to communicate zero-hour patterns.

- Payroll blames the benefits administration system for failing to capture the correct effective dates.

This administrative friction forces leadership to burn manual hours during Q1 trying to perform retroactive forensic investigations. Teams are left scrambling to track down store managers and historical shift schedules just to patch missing termination codes before transmission — a chaotic approach that still leaves room for human error.

Securing a Unified Compliance Record

Resolving the data distortion caused by high turnover demands a shift from manual data processing to an automated, integrated data stack. HR and compliance teams cannot afford to spend the first quarter of the year losing hundreds of hours running manual, forensic investigations to patch missing termination codes.

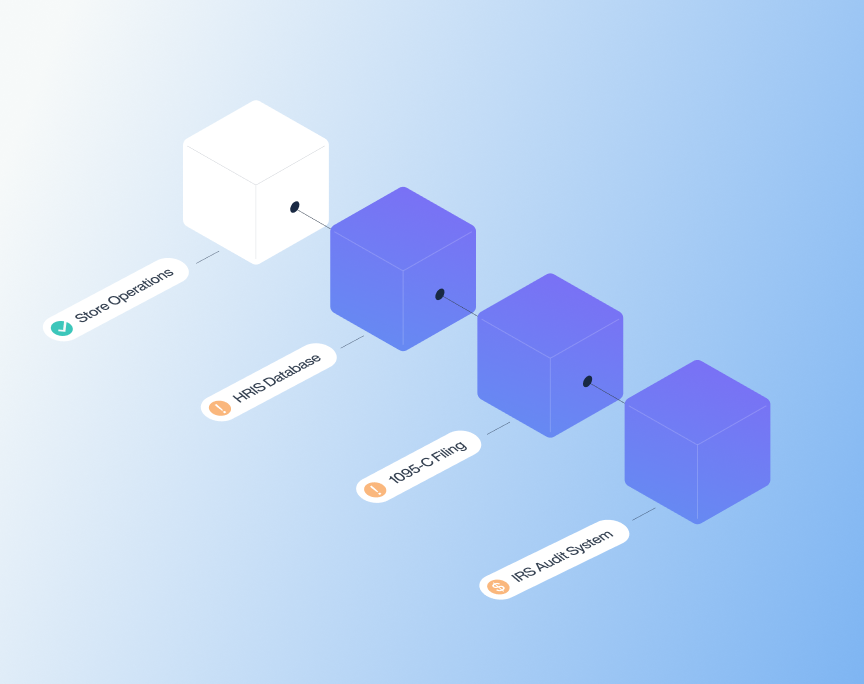

Establishing a unified record ensures that information streams from local time-and-attendance logs, benefit enrollment engines, and centralized payroll databases are reconciled proactively on a monthly basis.

When an employee’s hours drop to zero but no formal termination is logged, the discrepancy surfaces, allowing teams to isolate and fix ghost employee records weeks before filing.

Closing Ghost Employee Records Before They Reach the Filing

The blame cycle does not begin in January. It begins the moment a worker walks off a shift in October and nobody logs the separation.

Catching that discrepancy throughout the year — before it compounds into a multi-month coverage gap, conflicting 1095-C codes, and a Q1 investigation nobody has time for — is the whole point. Put “Ghost Employees” to rest with ACA Complete®.