ACA Reporting Compliance: The Complete Guide for Employers

ACA Compliance Landscape

What is the current state of ACA compliance for employers?

For the 2025 and 2026 tax years, the IRS has significantly increased enforcement through the Affordable Care Act Information Returns system.

Key regulatory shifts include a new 10-form electronic filing threshold and the Employer Reporting Improvement Act, which expanded the response window for IRS Letter 226J to 90 days.

This resource provides technical answers to the most common questions regarding the ACA Employer Mandate, full-time equivalent (FTE) calculations, and penalty mitigation.

- IRS enforcement through the AIR system

- New 10-form electronic filing threshold

- Letter 226J response window expanded to 90 days

- Employer Mandate, FTE calculations, and penalty mitigation

ACA Compliance Basics

Why data integrity is the standard for ACA Compliance

As IRS penalty assessments (ESRP) continue to rise — $3,340 per employee for IRC 4980(a) for the 2025 tax year — standard payroll exports and manual spreadsheets are no longer sufficient to prevent audits.

Modern ACA compliance requires a forensic approach to data to ensure 1095-C coding accuracy and affordability safe harbor application. This guide covers critical compliance queries:

-

ALE Identification

How to determine if you are an Applicable Large Employer. -

Affordability Thresholds

Navigating the move to 9.02% (2025) and 9.96% (2026) standards. -

FTE Calculations

The specific math for the Look-Back Measurement Method. -

IRS Penalty Defense

Step-by-step protocols for responding to Letter 226J and Letter 5699. -

State Mandates

Filing requirements for CA, MA, NJ, RI, and DC.

Does the ACA employer mandate apply to my company?

The federal tax code dictates that any organization qualifying as an Applicable Large Employer (ALE) must comply with the ACA Employer Shared Responsibility provisions.

If your workforce meets the federal threshold, you are legally required to offer Minimum Essential Coverage (MEC) to eligible full-time employees and their dependents. Failure to meet these federal mandates triggers automated enforcement and penalty assessments via the IRS AIR system.

Employer Mandate Basics:

-

Applicable Large Employer

50+ full-time and FTE employees -

Minimum Essential Coverage

Required for eligible full-time employees and dependents -

IRS AIR Enforcement

Missing coverage can trigger penalty assessments

How do I determine if my company qualifies as an ACA Applicable Large Employer?

An organization qualifies as an ALE if it employed an average of 50 or more full-time employees — including full-time equivalent (FTE) employees — during the preceding calendar year.

How do I calculate this threshold?

-

Aggregate Hours

Organizations must combine hours across all entities sharing common ownership (controlled groups). -

Monthly Averages

The status is determined by the average of monthly totals over the prior year. -

Seasonal Worker Exception

Employees working 120 days or fewer may be excluded from the ALE count under specific IRS seasonal worker rules.

ACA Reporting Requirements

How do I calculate full-time and full-time equivalent employees for ACA compliance?

The IRS defines a full-time employee as anyone averaging 30 hours per week or 130 hours per month. To calculate full-time equivalents (FTEs) on a monthly basis, follow these steps:

-

Identify Non-Full-Time Staff

List all employees not meeting the 130-hour monthly threshold. -

Aggregate Hours

Combine their total hours for the month, capping each employee at 120 hours. -

Divide by 120

Divide that aggregate total by 120 to find your FTE count for that month. -

Final Calculation

Add your FTE count to your total number of full-time employees.

Implementing the Look-Back Measurement Method provides a standardized framework for tracking variable-hour and seasonal workforces without triggering data misalignment.

What specific ACA compliant health coverage options do I need to include?

To satisfy the Employer Mandate and avoid Employer Shared Responsibility Payments (ESRP), ALEs must offer coverage that meets two specific criteria: Minimum Essential Coverage (MEC) and Minimum Value (MV).

The plan must cover at least 60% of the total allowed cost of benefits expected to be incurred under the plan. The data proving these offers must be coded and reported to the IRS.

-

Minimum Essential Coverage (MEC)

-

Minimum Value (MV)

-

60% of total allowed cost of benefits

How do I determine if the health coverage offerings meet ACA affordability requirements?

Affordability is a strict mathematical threshold set annually by the IRS. A plan is considered affordable if the employee’s required contribution for the lowest-cost, self-only coverage does not exceed the annual affordability percentage of their household income.

Because employers rarely know an employee’s exact household income, they must rely on highly specific federal safe harbors to prove compliance.

What ACA affordability safe harbors can employers use to reduce penalty risk?

The IRS provides three primary affordability safe harbors to insulate organizations from IRS enforcement:

-

W-2 Safe Harbor

Based on the wages reported in Box 1 of the employee's W-2. -

Rate of Pay Safe Harbor

Based on the employee's hourly rate or monthly salary at the start of the plan year. -

Federal Poverty Line Safe Harbor

Ensures the employee's contribution doesn’t exceed a set percentage of the FPL.

What are the IRS reporting requirements for ACA compliance and when are forms due?

ALEs must annually file Form 1094-C (the transmittal) and Form 1095-C (the employee statement) with the IRS.

Key deadlines and rules:

-

Employee Distribution

furnished -

IRS Filing

March 31 — Electronic filings are due to the IRS. -

Mandatory Electronic Filing

10 returns — The IRS mandates electronic filing for nearly all ALEs, as the threshold for paper filing has been lowered across all information return types.

Navigate the transmittal process with the supporting guides:

-

Employer's Guide to IRS Form 1094-C for ACA Compliance

Learn how the transmittal form supports ACA reporting.

-

Employer's Guide to Coding ACA Form 1095-C

Review employee statement coding requirements and best practices.

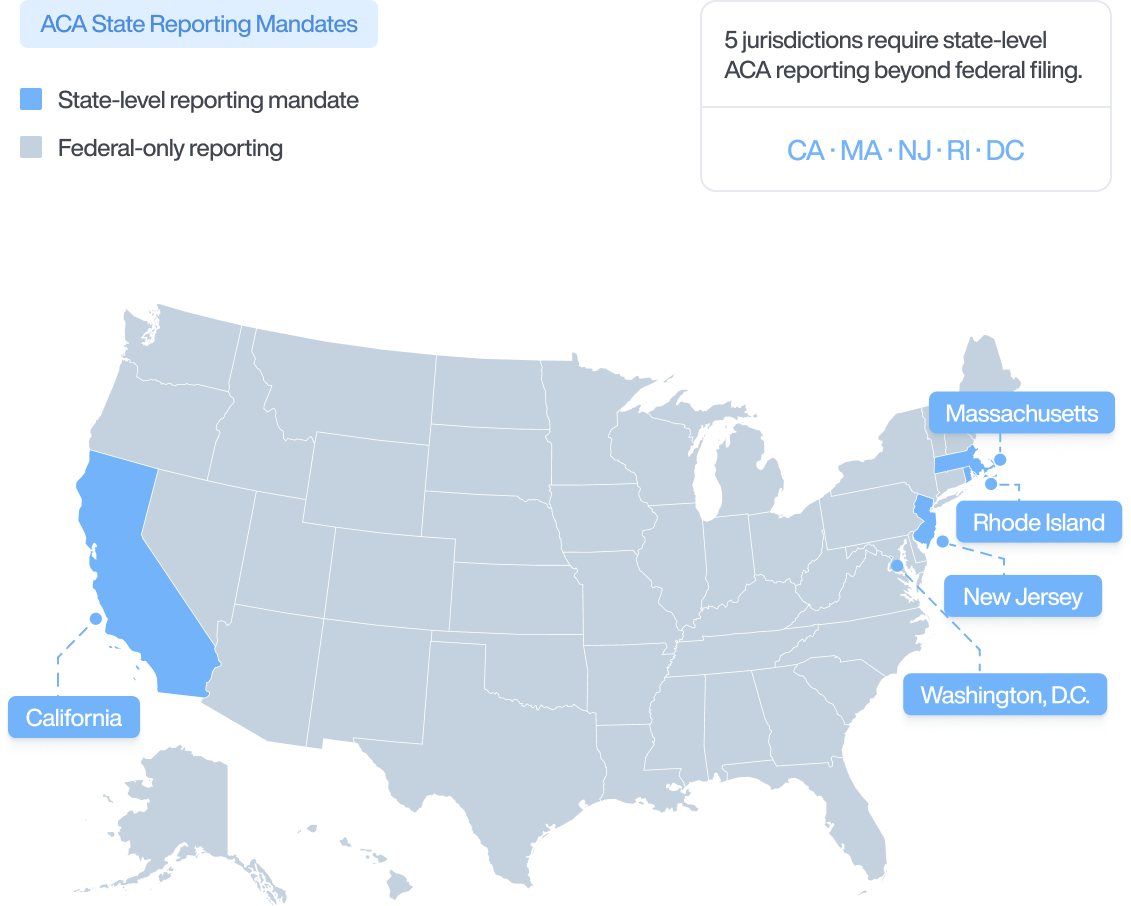

What Are the State-Level ACA Reporting Mandates?

Does my state have ACA reporting requirements beyond the federal mandate?

Satisfying the IRS AIR system represents only the baseline of employer obligation. Organizations with residents in the following jurisdictions must comply with independent state-level reporting requirements:

- California

- Massachusetts

- New Jersey

- Rhode Island

- Washington D.C.

These jurisdictions require independent data sets and unique filing deadlines, necessitating an automated approach to prevent state-level non-compliance penalties.

How Are IRS ACA Penalties Calculated?

What are ACA employer penalties for non-compliance?

The IRS uses the AIR (Affordable Care Act Information Returns) system to identify data discrepancies — such as an employee receiving a Premium Tax Credit (PTC) while their Form 1095-C indicates no affordable offer was made.

When a discrepancy is found, the IRS issues Letter 226J. This notice contains the proposed ESRP assessment. Under the Employer Reporting Improvement Act, employers now have a 90-day window (increased from 30 days) to dispute the proposed assessment.

-

4980H(a) Penalty

Triggered when an ALE fails to offer required Minimum Essential Coverage. -

4980H(b) Penalty

Triggered when coverage is offered but is unaffordable or does not provide minimum value.

How should employers prepare for an IRS ACA audit?

To successfully prepare for an IRS ACA audit, employers must transition from reactive year-end reporting to proactive, year-round data validation.

Because the IRS Affordable Care Act Information Returns (AIR) system uses automated data-matching to trigger penalty assessments, your audit defense relies entirely on the mathematical accuracy of your historical records.

To ensure audit readiness and survive federal scrutiny, ALEs must implement the following steps:

-

Eliminate Data Silos

Consolidate disparate HRIS, time-and-attendance, and benefits data into a single, verified source of truth. -

Conduct Pre-Filing Verification

Run logic checks on Form 1095-C prior to submission to ensure Line 14 (Offer of Coverage) and Line 16 (Safe Harbor) codes do not logically conflict. -

Document the Look-Back Method

Maintain unalterable, seamless historical data proving the precise hours of service for variable-hour, seasonal, and PRN employees.

Letter 226J is the IRS notice proposing an Employer Shared Responsibility Payment and giving employers a chance to respond.

Choose the path that matches your situation: immediate response or preventive planning.

-

Received a Letter 226J?

Understand the notice and prepare your response. -

Preparing for an ACA audit?

Organize your data and reduce penalty risk.

How to Simplify Your ACA Compliance Process

What is the most efficient way to manage ACA compliance as an employer?

The most effective risk management strategy is transitioning away from standard out-of-the-box software and manual spreadsheets. Certified bi-directional integrations provide the data integrity required to survive federal scrutiny.

By utilizing Trusaic, organizations gain access to pre-filing penalty risk analytics — identifying IRS penalty risks hidden within the 1095-C codes before the data goes to the IRS, ensuring audit-ready compliance records.

- Data integrity

- Penalty risk assessment

- Pre-filing penalty risk analytics

- 1095-C review

- Audit-ready compliance records