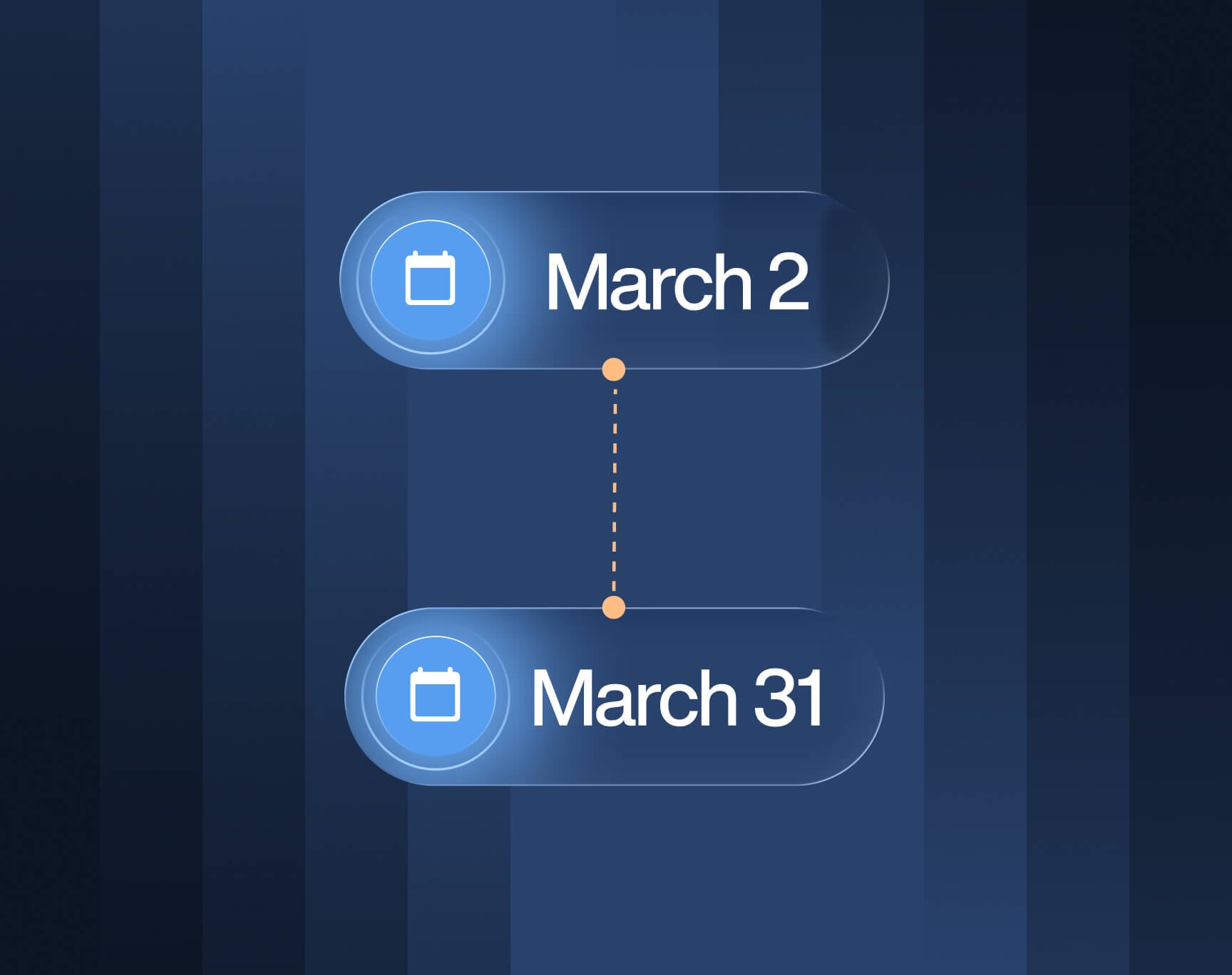

The federal deadline to electronically file Affordable Care Act (ACA) Forms 1094-C and 1095-C with the IRS is March 31, 2026. Applicable Large Employers (ALEs) must transmit this data via the IRS AIR system to prove compliance with the Employer Mandate for the 2025 tax year.

Furnishing forms to employees by March 2 was just step one; your true financial risk lies in the IRS transmission. Passing the IRS schema doesn’t guarantee compliance — a single coding contradiction can trigger massive penalty notices.

Use this final checklist to validate your data before hitting submit.

1. How to Validate Your IRS AIR System Transmission Readiness

The IRS has permanently lowered the electronic filing threshold to 10 or more returns of any type combined. This regulatory shift makes paper filing obsolete for virtually all ALEs. You must be prepared to transmit your data digitally.

- Verify your Transmitter Control Code (TCC): Ensure your organization’s TCC is active, up to date, and specifically authorized for ACA Information Returns (AIR) for the current filing year.

- Test your XML formats: Confirm that your reporting software can successfully generate the XML schema required by the IRS AIR system. Failing to meet these structural requirements will result in a rejection.

2. How to Reconcile Form 1094-C and 1095-C Data for the IRS

The IRS’s automated ACA Compliance Validation (ACV) system flags discrepancies between your high-level transmittal summary (Form 1094-C) and the individual employee forms (Form 1095-C).

- Match the Headcount: Ensure the total number of 1095-C forms generated perfectly matches the full-time employee count reported in Part III, Column (b) of your authoritative 1094-C.

- Verify the 95% Offer Box: Confirm that Part III, Column (a) is checked Yes for all applicable months. Failing to check this box acts as an automatic admission of non-compliance and will trigger a devastating Section 4980H(a) penalty.

3. Audit Form 1095-C Codes to Prevent IRS Penalty Triggers

Incompatible codes on Form 1095-C Lines 14 and 16 tell a conflicting compliance story. These logical errors often trigger an automated 4980H(b) penalty assessment if the employee in question received a Premium Tax Credit (PTC) from a state or federal exchange.

- Audit for the 1E / Blank Error: Did you report a qualifying offer of coverage to an employee (Code 1E on Line 14) but fail to input a corresponding safe harbor code on Line 16? This data gap leaves you vulnerable to penalty logic.

- Audit for the 1H / 2G Error: Are you attempting to claim a Federal Poverty Line safe harbor (Code 2G) for an employee who was never actually offered coverage (Code 1H)? The IRS systems will catch this contradiction.

4. Navigate Staggered State-Level ACA Mandates

Securing your federal transmission does not absolve your organization of state-level individual mandate reporting requirements — and importantly, not all state deadlines align with the federal March 31 calendar.

- Identify State Residents: Isolate your workforce data for any employees residing in California, New Jersey, Rhode Island, or Washington D.C.

- Format Conversion: Convert your federal XML data into the unique file formats and schemas required by those specific state revenue departments. A standard IRS file will almost always be rejected by state portals.

- Track Staggered Deadlines: Ensure you are tracking toward the distinct filing deadlines for each required state jurisdiction.

- March 31: New Jersey, Rhode Island

- April 30: Washington D.C.

- May 31: California extended deadline

5. How to File Form 8809 for an ACA Reporting Extension

If your final data audit reveals massive gaps, missing codes, or irreconcilable logic, do not rush a flawed filing just to hit the March 31 deadline.

- Determine Data Viability: Calculate the risk of filing as-is versus requesting an extension. Submitting cleanly formatted but legally inaccurate data is riskier than securing a brief extension to fix it.

- File Form 8809: If you need more time, submit Form 8809 before March 31 to secure an automatic 30-day extension from the IRS.

- Execute a Forensic Audit: Use this 30-day window strictly to definitively correct coding errors, recalculate employee eligibility, and ensure data integrity before your final submission.

How Trusaic Ensures a Successful March 31 ACA E-Filing Submission

Meeting the March 31 ACA electronic filing deadline is about more than just getting a file accepted by the IRS AIR system — it is about ensuring the data you submit is substantively accurate to prevent costly IRS penalty notices.

Trusaic transforms this high-stakes filing event from a reactive scramble into a secure, mathematically defensible operation.

- Proprietary Penalty Risk Assessment: We do not just run your data through a basic schema checker. Our system forensically audits your 1094-C and 1095-C logic to catch the false positive coding errors that trigger Section 4980H penalties before you hit submit.

- Seamless State Filing Integration: We automatically execute the federal-to-state XML format conversions required for your employees in California, New Jersey, Rhode Island, and D.C., ensuring you meet every overlapping mandate.

- Expert Oversight: Our designated ACA compliance specialists review your data and manage the final transmission, giving you audit-ready confidence rather than filing-season anxiety.

Don’t leave your March 31 filing to chance. Contact Trusaic today to ensure your ACA data is accurate, compliant, and securely transmitted.