The Employer Reporting Improvement Act of 2024 (H.R. 3801) signals a major shift in how the IRS handles Affordable Care Act (ACA) enforcement.

While the legislation includes practical administrative updates — extending the employer response window for Letter 226J to 90 days — a critical change for HR and finance leaders is the establishment of a six-year statute of limitations for Employer Shared Responsibility Payment (ESRP) assessments.

Here is how this new timeframe changes the audit landscape, the operational implications for your business, and the steps your organization should take to maintain compliance.

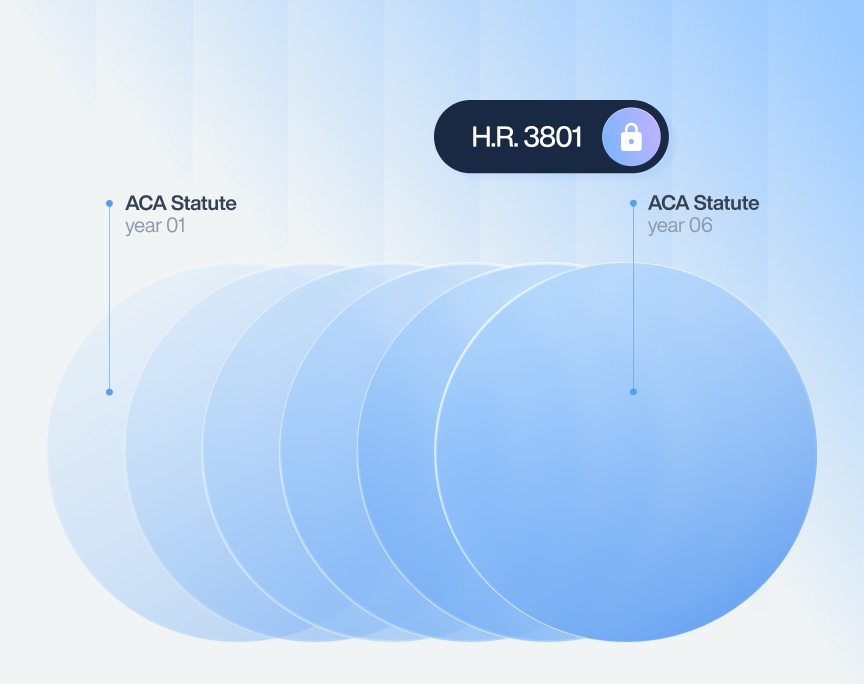

The 6-Year ACA Statute of Limitations

Under H.R. 3801, the IRS now has exactly six years from the due date of an employer’s ACA information returns (Forms 1094-C and 1095-C) — or the date those returns were actually filed, whichever is later — to propose an ESRP assessment.

For employers, this establishes a clear, statutory timeframe for ACA compliance liability. It effectively replaces the previous lack of a defined compliance window with a structured, predictable timeline that organizations can build their data retention policies around.

Before vs. After H.R. 3801: The Changing Audit Landscape

The Before

Prior to this legislation, the IRS maintained the position that no statute of limitations applied to ESRP assessments under Section 4980H of the tax code. Because the agency viewed these assessments differently from standard tax returns, they retained the authority to audit reporting years indefinitely.

This required employers to manage, store, and maintain complex compliance data from as far back as 2015, creating a significant and ongoing administrative burden for HR and payroll departments.

The After

H.R. 3801 officially alters this regulatory dynamic. After six years, the IRS can no longer legally issue an ESRP assessment for that specific reporting year. While employers must still adhere to rigorous record-keeping standards to prove they offered affordable minimum essential coverage, they now have a concrete timeline for data retention and compliance management.

What Are the Implications for HR and Finance

The transition to a formal six-year cap creates several positive operational shifts for enterprise organizations:

- Clarity in Risk Management: Without an open-ended audit window, finance and compliance teams can establish a predictable, rolling schedule for managing historical risk. It allows leadership to understand exactly which tax years are subject to review and which are officially closed.

- Streamlined Data Management: Managing HR data across different platforms, software updates, and vendors over a decade is incredibly challenging. The new cap allows organizations to focus their data security and retention efforts strictly on the required six-year window, reducing the administrative strain of maintaining obsolete systems or outdated spreadsheets.

- Defined Enforcement Parameters: Because the IRS now operates within a strict six-year timeframe, employers must ensure their data is highly accurate and readily accessible during this period. The agency has a clear window to conduct its compliance reviews, making it essential that your data is always audit-ready.

How Can Employers Use This Statute of Limitations Today?

To align internal processes with these new regulatory parameters, employers should focus on implementing these core compliance strategies:

- Update Data Retention Policies: Adjust your corporate data retention schedules to reflect the new law. Ensure that all Forms 1094-C and 1095-C, raw payroll data, and proof of coverage offers are securely archived and easily accessible for a minimum of six full years from the filing date.

- Perform Regular Internal Audits: Use this defined timeline to establish a routine cadence for internal compliance reviews. Proactively identifying and resolving coding inconsistencies ensures your data is accurate and compliant before the IRS ever reviews it.

- Consolidate Compliance Data: Transition historical ACA data from disparate legacy systems into a centralized, secure platform. If the IRS requests documentation for a year within the active statute of limitations, having a single source of truth significantly streamlines the response process and ensures no data is lost during vendor transitions.

How Trusaic Can Help You Navigate the Change

While a six-year limit on IRS audits provides welcome regulatory clarity, maintaining compliance throughout that period still requires flawless data management. Trusaic’s ACA Complete® platform actively cleanses and validates your workforce data year-round, ensuring that your filings are logically sound and mathematically defensible.

If the IRS challenges a filing within the statute of limitations, our specialized Penalty Response service manages the correspondence from start to finish. We utilize your validated historical data to resolve inquiries and definitively eliminate proposed ESRP assessments.

Secure your historical data and maintain proactive compliance.